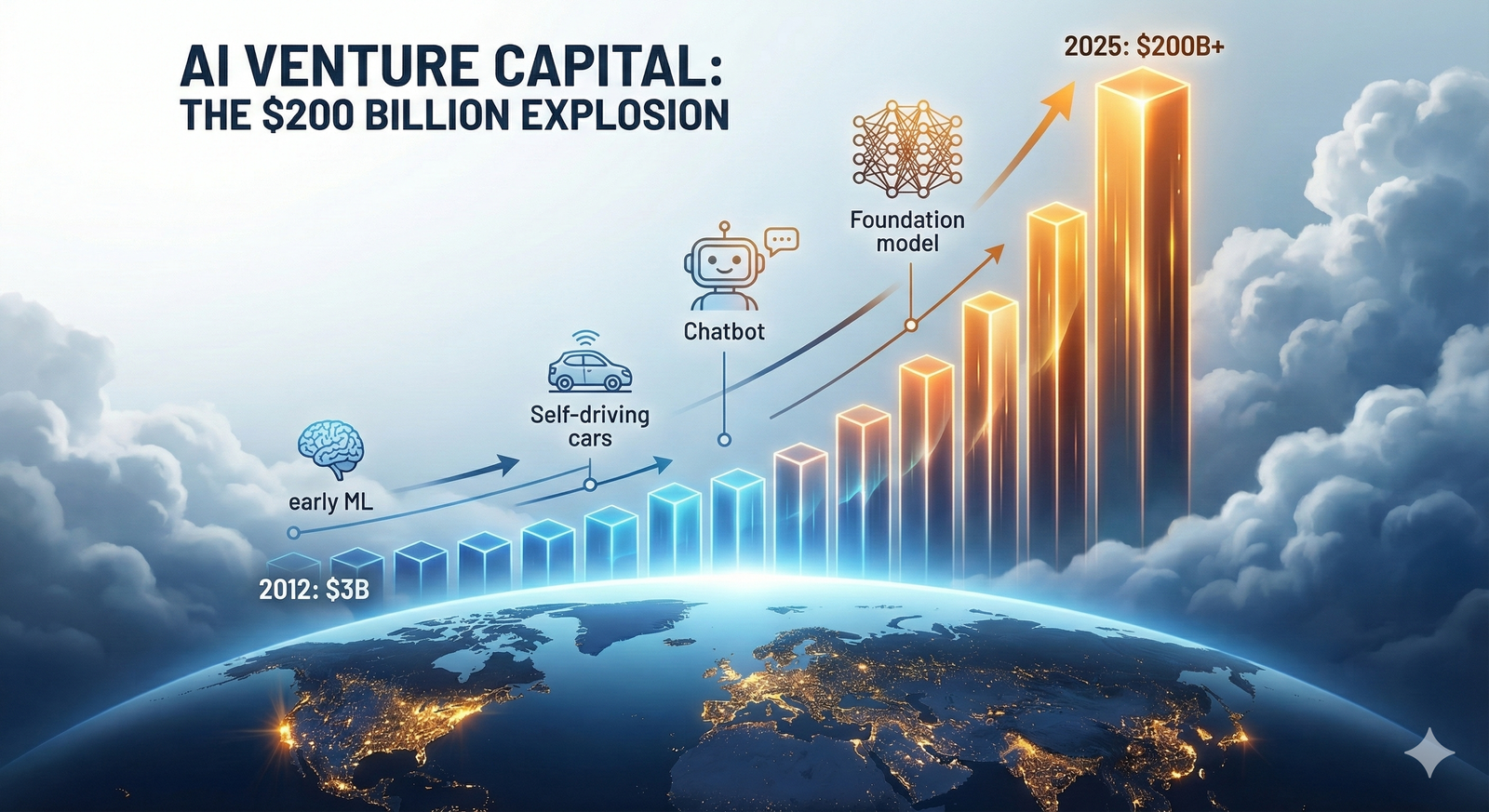

AI Venture Capital Exploded from $3 Billion to $200 Billion in a Decade

Venture capital investment in AI has surged 67-fold since 2012, now capturing nearly half of all global VC funding. We analyze the transformation that reshaped the entire venture landscape.

Giuseppe Gaspari

The $200 Billion Explosion

From a $3B niche to half of global venture capital. Click any milestone to jump to that section.

The Humble Beginning

Global AI funding sits at just $3 billion. The sector is a niche largely ignored by mainstream VC.

The DeepMind Watershed

Google acquires DeepMind for ~$650M. This sparks the first "AI Talent War" among Big Tech firms.

The Autonomous Vehicle Hype

AVs dominate deals, attracting $95B cumulatively. Peak hype reaches $12.5B in 2021 before the sector collapses.

The ChatGPT Spark

OpenAI launches ChatGPT. It hits 1M users in 5 days, triggering the greatest capital reallocation in VC history.

Microsoft & The Surge

Microsoft invests $10B in OpenAI. Despite a global VC downturn, AI captures 18% of all venture funding.

The $200 Billion Era

AI funding hits $202.3B. OpenAI valued at $500B. AI now captures 50% of all global venture dollars.

Total Growth 2012–2025

Venture capital investment in artificial intelligence has undergone a transformation unlike any in technology history. What began as $3 billion in global AI funding in 2012 has surged to over $200 billion in 2025—a staggering 67-fold increase that has reshaped the entire venture landscape [1][2].

AI now captures nearly half of all global venture capital, up from just 14% five years ago [1]. This concentration represents both the largest technology bet in VC history and, according to some skeptics, the greatest test yet of whether capital markets can accurately price transformative innovation.

The Early Years Established Foundation for Explosive Growth

The first wave of AI venture investment, from roughly 2010 to 2015, was remarkably modest by today's standards. In 2010, AI startups attracted just $45 million globally, with average early-stage rounds hovering around $5 million [3]. By 2015, total annual investment had grown to $310 million—nearly sevenfold growth, yet still a rounding error compared to what followed [4][5].

During this period, machine learning infrastructure and natural language processing dominated deal flow. Sentient Technologies raised a notable $103.5 million Series C in 2014, while Khosla Ventures, Data Collective, and Intel Capital emerged as the most active AI investors [6]. Approximately 65% of deals went to seed and Series A rounds, and 93% of funding concentrated in California, establishing the Bay Area's enduring dominance in AI [7].

The DeepMind Acquisition

Google's $500-650 million acquisition of DeepMind in January 2014 proved a watershed moment [8]. The deal, which outbid Facebook for a pre-revenue UK research lab, demonstrated that AI companies could command premium valuations based purely on talent and research capability [9]. This acquisition sparked an "AI talent war" among Big Tech firms that continues today.

Autonomous Vehicles Dominated Mid-Decade Before Collapse

From 2015 to 2021, autonomous vehicles became the largest AI investment category by far, attracting $95 billion cumulatively between 2012 and 2020 [10]. At its peak in 2021, AV startups raised $12.5 billion across 264 deals [11]. U.S. and Chinese companies captured 98% of this investment [10].

The sector's trajectory illustrates how quickly VC sentiment can shift. Argo AI, despite raising $2.6 billion from Ford and Volkswagen, shut down entirely in October 2022 [12]. GM halted Cruise robotaxi funding in December 2024 after investing $16 billion total [13]. Public market performance proved equally brutal: 14 AV-related IPOs saw average declines exceeding 80% post-debut [14]. As PitchBook analyst Jonathan Geurkink observed, VCs have largely abandoned the vertical due to dismal public market performance of EV and autonomous driving companies [13].

The Casualties

Argo AI shut down entirely in October 2022 despite raising $2.6 billion from Ford and Volkswagen. GM halted Cruise robotaxi funding in December 2024 after investing $16 billion total. 14 AV-related IPOs saw average declines exceeding 80% post-debut.

ChatGPT's Launch Triggered the Greatest Capital Reallocation in VC History

The November 30, 2022 launch of ChatGPT fundamentally altered AI investment patterns. OpenAI's chatbot reached one million users within five days—the fastest consumer technology adoption ever recorded—and triggered an immediate capital surge into generative AI [16].

Within two months, Microsoft invested $10 billion in OpenAI [17]. By mid-2023, 18% of all global venture funding was flowing to AI companies despite a broader market downturn [18][19]. By late 2024, that figure reached 33%, and by 2025, AI captured a remarkable 50% of global VC dollars [20][1].

The numbers tell a stark story of before and after. Global AI venture investment stood at roughly $91.9 billion in 2022. It rose modestly in 2023 as the broader market corrected but with AI as the clear bright spot, then exploded to $100-114 billion in 2024—an 80-100% year-over-year increase [21][22]. In 2025, according to Crunchbase data, AI startups raised $202.3 billion, another 75% jump that set new records [2].

Generative AI specifically grew from approximately $4 billion in 2022 to $33.9 billion in 2024—an 8.5x increase—and reached $49.2 billion in the first half of 2025 alone, already exceeding all of 2024 [23].

| Year | Global AI VC | GenAI Funding | AI Share of VC |

|---|---|---|---|

| 2022 | ~$92B | ~$4B | ~18% |

| 2023 | ~$95B | ~$25B | ~25% |

| 2024 | ~$114B | ~$34B | ~33% |

| 2025 | $202B | $49B+ (H1) | ~50% |

Foundation Models Versus Applications Creates a Strategic Divide

The generative AI boom has split venture investment into two distinct camps: foundation model companies building large language models and application-layer startups deploying those models for specific use cases.

Foundation model companies have attracted extraordinary capital. In 2025, foundation model firms raised $80 billion—representing 40% of all global AI funding—more than double the prior year's total [2][24]. OpenAI alone raised $40 billion from SoftBank in March 2025, achieving a $500 billion valuation that made it the most valuable private company ever [25]. Anthropic reached a $183 billion valuation after raising $13 billion in September 2025, with revenue reportedly growing from $1 billion to $5 billion ARR within a single year [26][27]. Elon Musk's xAI raised $20 billion in January 2026 at a $230 billion valuation [28].

The scale is remarkable: OpenAI and Anthropic alone captured 14% of all global venture investment in 2025 [2][29].

| Company | Latest Raise | Valuation |

|---|---|---|

| OpenAI | $40B (SoftBank, Mar 2025) | $500B |

| xAI | $20B (Jan 2026) | $230B |

| Anthropic | $13B (Sep 2025) | $183B |

Application-layer companies, while raising smaller absolute amounts, have demonstrated faster market traction. According to Menlo Ventures, enterprise AI application spending reached $19 billion in 2025, with startups capturing 63% market share versus incumbents—a complete reversal from 2024 [30][31]. AI coding tools emerged as the breakout category, growing from $550 million in 2024 to $4 billion in 2025 [32]. Cursor, the AI code editor, reached $200 million in revenue before hiring a single enterprise salesperson and achieved a $29.3 billion valuation [33][34].

AI Coding Tools: The Breakout Category

AI coding tools grew from $550 million in 2024 to $4 billion in 2025. Cursor, the AI code editor, reached $200 million in revenue before hiring a single enterprise salesperson and achieved a $29.3 billion valuation.

Healthcare and Vertical AI Emerge as Foundation Model Alternatives

As some investors question whether foundation model valuations have become stretched—OpenAI trades at roughly 167x revenue versus 5-10x for mature SaaS—capital has increasingly flowed toward vertical AI applications [35].

Healthcare AI attracted $4 billion in the first half of 2025, comprising 62% of all digital health venture funding [36]. Ambient scribes—AI tools that document patient encounters—became a $600 million market with multiple unicorns including Abridge and Ambience [37]. Drug discovery AI continued its rise, with Xaira Therapeutics raising a $1 billion Series A [38].

Legal AI similarly accelerated, with Harvey raising multiple $300 million rounds to reach a $5 billion valuation. Vertical AI across healthcare, legal, finance, and government totaled $3.5 billion in 2025—triple the prior year [39][40].

Sequoia partner Sonya Huang articulated the investment thesis: application categories remain a largely unexplored opportunity space compared to the more established model and infrastructure segments [41].

- Healthcare AI: Attracted $4 billion in H1 2025, comprising 62% of all digital health venture funding.

- Ambient Scribes: Became a $600 million market with multiple unicorns including Abridge and Ambience.

- Drug Discovery: Xaira Therapeutics raised a $1 billion Series A.

- Legal AI: Harvey raised multiple $300 million rounds to reach a $5 billion valuation.

The Market Shows Maturation, Not Cooling

Despite record aggregate funding, several metrics suggest the AI market is maturing rather than simply expanding. The number of generative AI deals actually fell from 273 in 2023 to 171 in 2024, even as total capital increased [42]. Early-stage AI funding declined 12-14% year-over-year in 2024 [43]. Average deal sizes tripled, with late-stage generative AI rounds averaging $1.55 billion in the first half of 2025 versus $481 million in 2024 [44].

This concentration accelerated dramatically: the top 10 AI companies captured 51% of all AI investment in 2024 [45]. Fifteen companies secured funding rounds exceeding $2 billion in 2025 alone [46].

VCs are becoming more selective, favoring proven revenue models over pure research. Enterprise AI adoption provides justification: 78% of organizations now use AI, up from 55% in 2023, with users reporting average 40% productivity gains [47]. Menlo Ventures argues the data signals a boom versus a bubble [30].

Looking toward 2026, market observers anticipate continued growth but with important evolution. Agentic AI—autonomous systems that can execute multi-step tasks—is projected to grow from under $1 billion in 2024 to $51.5 billion by 2028 [48][49]. Both OpenAI and Anthropic are reportedly preparing IPO filings, which would provide the first public market tests of generative AI valuations [50][51].

Geographic Concentration Intensifies

North America, and specifically the San Francisco Bay Area, has captured an increasingly dominant share of AI investment. In 2025, U.S. companies attracted $159 billion, representing 79% of global AI funding [52][53]. The Bay Area alone accounted for $122 billion—more than the rest of the world combined [2]. U.S. private AI investment was 12 times greater than China's $9.3 billion and 24 times greater than the UK's $4.5 billion [54][55].

| Region | 2025 AI Funding | Global Share |

|---|---|---|

| United States | $159B | 79% |

| Bay Area alone | $122B | 60% |

| China | $9.3B | ~5% |

| United Kingdom | $4.5B | ~2% |

This concentration reflects both the location of major foundation model companies and the continued gravitational pull of established AI talent networks. All six billion-dollar-plus rounds in Q2 2025 went to U.S.-based companies [2].

The transformation from a $3 billion niche in 2012 to a $200 billion sector commanding half of all venture capital represents the fastest and largest capital reallocation in VC history. Whether this concentration will yield commensurate returns—or whether future observers will view 2024-2025 as a period of irrational exuberance—remains the defining question for technology investors.

References

- Techbuzz. "AI Startups Capture Over Half of All VC Money for First Time."

- Crunchbase News. "6 Charts That Show The Big AI Funding Trends Of 2025."

- CB Insights. "A New High In Deal Activity To Artificial Intelligence Startups In Q4'15."

- CB Insights. "A New High In Deal Activity To Artificial Intelligence Startups In Q4'15."

- CB Insights. "A New High In Deal Activity To Artificial Intelligence Startups In Q4'15."

- CB Insights. "A New High In Deal Activity To Artificial Intelligence Startups In Q4'15."

- CB Insights. "Artificial Intelligence Explodes: New Deal Activity Record For AI."

- Wikipedia. "Google DeepMind."

- Fortune. "The Google Brain-DeepMind merger is probably good for Google. It might not be for us."

- OECD AI. "A sharp increase in AI-related venture capitalist investments."

- Crunchbase News. "Autonomous Vehicle Funding Stuck In Neutral."

- OECD AI. "A sharp increase in AI-related venture capitalist investments."

- PitchBook. "Mobility tech VC funding steers toward 6-year low."

- Crunchbase News. "Self-Driving Tech Startups Are Driving Off A Cliff On Public Markets."

- Phoenix Strategy Group. "Investment Opportunities in Self-Driving Startups."

- Carta. "AI Startups Prevail in VC Market Downturn."

- Bloomberg. "Microsoft to Invest $10 Billion in ChatGPT Maker OpenAI."

- AI Business. "Generative AI Funding Hits $25.2 Billion in 2023, Report Reveals."

- Quartz. "Even the ChatGPT-fueled AI boom couldn't offset a slide in venture funding."

- Statista. "AI Sucks Up a Growing Chunk of VC Funding in the U.S."

- Inc. "Venture Capital Is Bouncing Back, but Not for Everyone."

- Harvard Business Review. "How Generative AI Is Reshaping Venture Capital."

- EY. "Generative AI VC Funding Hits $49.2B Globally in H1 2025."

- Tech Funding News. "$84B story: The 10 AI mega-rounds that defined 2025."

- Euronews. "ChatGPT maker OpenAI sees historic funding round."

- Anthropic. "Anthropic raises Series F at $183B post-money valuation."

- Goldman Sachs Asset Management. "Anthropic Raises $13B Series F."

- CNBC. "Elon Musk's xAI raises $20 billion from investors."

- Stifel Bank. "A Founder's Guide to the 2025 AI Landscape: Part Two."

- Menlo Ventures. "2025: The State of Generative AI in the Enterprise."

- Menlo Ventures. "2025: The State of Generative AI in the Enterprise."

- Menlo Ventures. "2025: The State of Generative AI in the Enterprise."

- Tech Funding News. "$84B story: The 10 AI mega-rounds that defined 2025."

- Fortune. "As AI investors fret over ROI, these startups attracted serious cash."

- Wiss. "OpenAI Valuation: What Tech Founders Need to Know."

- Fierce Healthcare. "Healthcare AI rakes in nearly $4B in VC funding."

- Menlo Ventures. "2025: The State of Generative AI in the Enterprise."

- DelveInsight. "AI Healthcare Startups: Investment & Funding Trends."

- Techbuzz. "49 US AI startups raised $100M+ in 2025."

- Menlo Ventures. "2025: The State of Generative AI in the Enterprise."

- Gene Dai. "Sonya Huang: Sequoia's AI Application Bet."

- S&P Global. "GenAI funding hits record in 2024."

- Mintz. "The State of the Funding Market for AI Companies: A 2024-2025 Outlook."

- EY. "Generative AI VC Funding Hits $49.2B Globally in H1 2025."

- CDP Center. "Venture investments in startups, scale-ups and AI: 2024-2025."

- Crunchbase News. "These Were The Largest Funding Rounds Of 2025."

- Menlo Ventures. "2025: The State of Generative AI in the Enterprise."

- MachineLearningMastery. "7 Agentic AI Trends to Watch in 2026."

- Ropes & Gray LLP. "Artificial Intelligence Q3 2025 Global Report."

- TechCrunch. "Anthropic reportedly raising $10B at $350B valuation."

- Foundation Capital. "Where AI is headed in 2026."

- Fullview. "200+ AI Statistics & Trends for 2025: The Ultimate Roundup."

- Stanford HAI. "The 2025 AI Index Report."

- Stanford HAI. "Economy | The 2025 AI Index Report."

- Stanford HAI. "Economy | The 2025 AI Index Report."

Giuseppe Gaspari

Founder & Editor of Will It Bubble. Cutting through the AI hype to share what actually matters.